Author: Franklin J. Parker

-

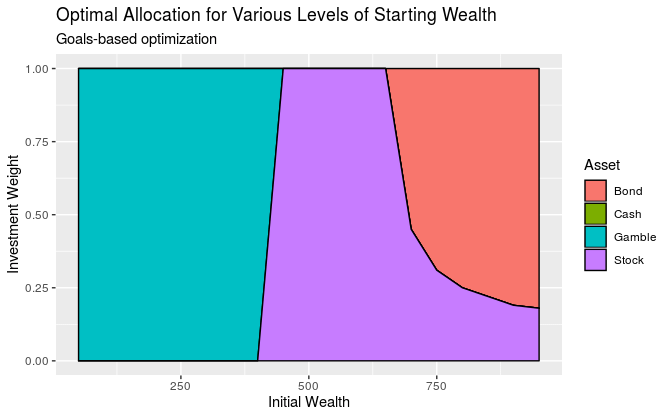

Allocating Wealth Both Across Goals and Across Investments

How to optimize wealth across your goals, as well as to investment portfolios within each of your goals. Supplement to Chapter 3 of my book, Goals-Based Portfolio Theory.

-

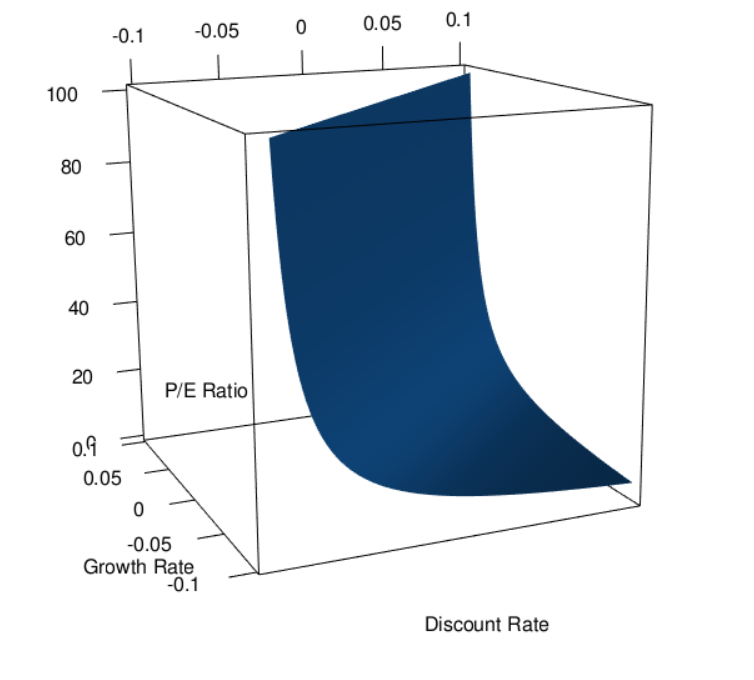

What Does the P/E Ratio Tell You About Investor Expectations?

Price to earnings ratios are readily observable, but what can they tell us about a market or security?

-

The Return Distribution of Bitcoin

A look at daily and monthly bitcoin return distributions. Which distribution best describes the observed data. And, what does this mean from a portfolio management perspective?

-

Wealth Management in the Algocen Era: A Speculative Future

What does investing look like in 2038?

-

Bernoulli’s Prisoner’s Dilemma: A Goals-Based Perspective

In 1738, the Swiss mathematician and physicist Daniel Bernoulli proposed a simple thought experiment: “A rich prisoner who possesses two thousand ducats but needs two thousand ducats more to repurchase his freedom, will place a higher value on a gain of two thousand ducats than does another man with less money than he.” Let’s continue to play this…

-

A Goals-Based View of Security Prices and Market Dynamics: WHAT IF THERE IS NO “CORRECT” MARKET PRICE?

I have been thinking lately about how a market of goals-based investors might interact. As it turns out, the resulting dynamics are rather interesting and not as simple as one might expect. Goals-based utility theory postulates that investors (of all types) interact with capital markets with specific objectives in mind (see Parker 2020). Investors seek…

-

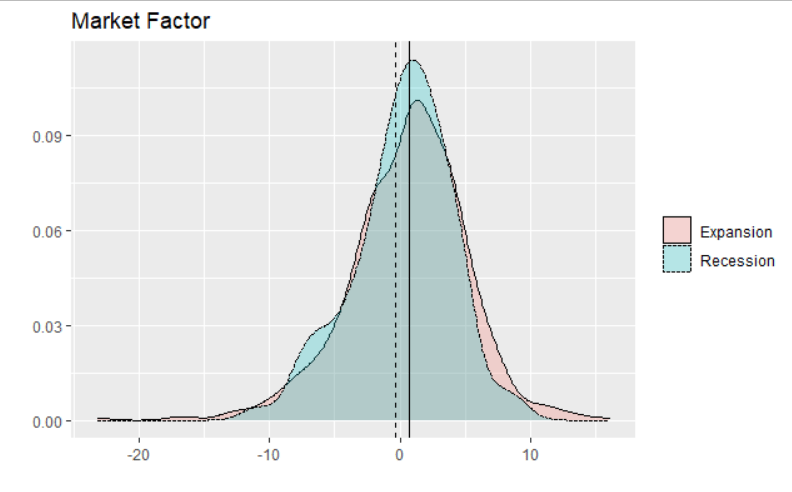

Five Factors Across the Business Cycle

Probably the most popular models in modern investment management are factor models. Growing out of the Capital Asset Pricing Model (CAPM), factor models were first theorized in Arbitrage Portfolio Theory and the concept was expanded and applied to risk premiums by Nobel-laureate Eugene Fama and Kenneth French (French, surprisingly, did NOT win a Nobel prize).…

-

On Horses, Tractors, and Markets

Growing up on a cattle ranch in central Texas, I developed a certain respect for the tools of the trade. Horses, tractors, trucks, trailers, bailing wire, and duct tape we all daily-use items for us. Each tool has its purpose, of course, and each tool has advantages and disadvantages for a particular job. Take, for…

-

Recession Forecasting with a Neural Net in R

I spend quite a bit of time at work trying to understand where we are in the business cycle. That analysis informs our capital market expectations, and, by extension, our asset allocation and portfolio risk controls. For years now I have used a trusty old linear regression model, held together with bailing wire, duct tape,…

-

How to Optimize a Goal-Based Portfolio

Traditional portfolio optimization (often called modern portfolio theory, or mean-variance optimization) balances expected portfolio return with expected portfolio variance. You input how opposed you are to portfolio variance (your risk tolerance), then you build a portfolio that gives you the best return given your risk tolerance. Goals-based investing, by contrast, defines “risk” as the probability…